Are We Due?

With the S&P 500 down 18.1% in 2022, it was the largest decline in the S&P 500 since 2008.

It was a challenging year to say the least. Looking at the Market Pulse you will notice nearly all our major indices were lower. The reason was not only due to a reset in stock valuations, but rising interest rates caused bond prices to fall, whereas bonds are typically a haven. The only true haven last year was commodities (we own a 4% gold weighting in our managed accounts) and cash.

Looking forward we can’t help but wonder will it be another down year, due to high inflation, a potential drop in corporate earnings and Fed Policies that are tightening, or will we see a rebound like 2009 where the S&P 500 ended up 26%.

Clients ask us all the time what we think the market will do and we know that predicting what the market will do this year is a futile exercise. What we can tell you is that the market on average is up 74% of the time, and in the 3rd year of a Presidential term we typically see the best average market performance, which is 13.5% vs a 6.7% in the first year, 4.3% in the second year and 7.4% in the fourth year.

Either way, we all look forward to what the New Year will bring.

Tax Season is Upon Us

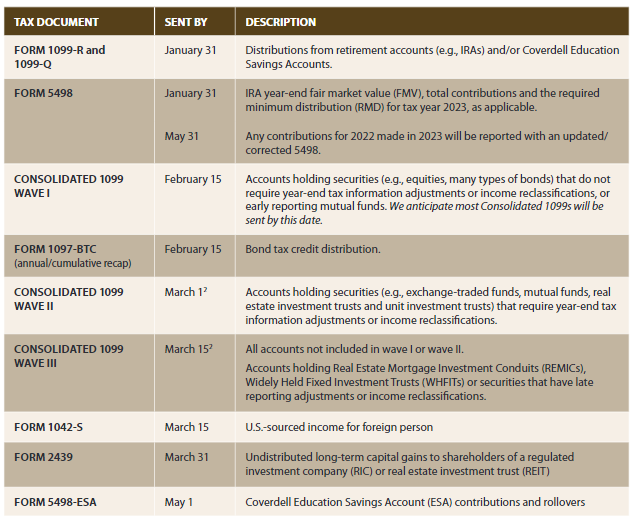

As we head into the heart of tax season, we want to provide you with the schedule of Baird’s 2022 Tax Document Mailing Schedule.

Last year was the first-year clients could elect to receive their tax documents electronically with an email notification as opposed to regular mail. Please double check how you receive your mailings, you may have elected to have your tax documents electronically sent to you.

Secure Act 2.0

Major changes occurred to retirement planning at the end of 2022 because of the passing of the $1.7 trillion-dollar omnibus government spending bill. Within that bill was a section called “Secure Act 2.0”, which was updates and enhancements to the 2019 bill.

While there were many updates, and we’d be happy to send you our Baird summary, we find these to be the most impactful for our clients.

- Secure Act 2.0 raised the IRA and required minimum distribution age from 72 to 73. In addition, the current law states that age increases again in 2033 to age 75. The bill still allows you to defer your first year’s distribution to April 1st of the year after you turn 73, however that means you’ll need to take two distributions that year.

- The bill makes two changes to rules surrounding qualified charitable distributions (IRA distributions directly to a charity). First is that the $100,000 QCD limit will be adjusted for inflation beginning in 2024. Secondly, you will now be allowed to make a “split interest” gift, which is a gift to a charitable remainder trust or charitable gift annuity. There are several limitations to these gifts, so if you plan to make a gift of this nature, please give us a call.

- The bill includes the ability to transfer funds from a 529 college savings account into a ROTH IRA beginning in 2024. There are limitations, such as, the beneficiary of the 529 must be rolled into a same name ROTH IRA. The maximum rollover amount is limited to the contribution limit for that year (currently $6,500 for 2023), that rollover reduces the contribution amount and there is a lifetime maximum rollover of $35,000. The 529 plan must also be opened for at least 15 years as of the date of the rollover.

There are several other changes to employee retirement accounts, conservation easements, ABLE accounts, and ESOPs. If you would like a more information on other highlights of the Secure Act 2.0, feel free to give us a call.

2023 Outlook and Thoughts on the Market

Making market predictions and guesses on where the market will end up this year is a futile exercise that we are consistently asked to do. I always make the joke, if we knew I would have been long retired and have my own private island, which is the reason I am still working.

Despite that, we know clients look to us for guidance as to what is occurring in the markets and how it might impact their accounts and investment portfolios. So, these are some of the factors that we think will play out over the course of the year and items to pay attention to.

- We cannot underestimate the power of the Federal Reserve and it’s its impact on the markets. We have not seen the Fed raise rates this quickly and tighten their monetary policy and this is likely to create a challenging equity market this year as all indications show they will likely continue to increase rates as inflation remains high.

- Many strategists believe that there is a high probably of recession, which historically has been described as two consecutive quarters of declining GDP. We wouldn’t entirely see this as a bad thing for the markets at they tend to bottom before or as the recession starts and recover before the recession ends.

- We would expect to see increased layoff announcements and corporate earnings decreasing this year. Compensation tends to be the highest expense for any corporation and to manage earnings, layoffs can be a fast and “effective” way to manage costs in a company. In turn, layoffs will likely bring down inflation as those out of work will decrease the demand for goods, which is one cause of higher inflation. While we never think layoffs are a good thing for the economy or individuals, the strong labor market likely needs to ease for companies to manage their earnings and inflation to decline.

- Presidential Cycles Matter…and they don’t. We have shared numerous times that the makeup of the government doesn’t directly indicate how a market will perform. In every year of a presidential term the markets average a positive rate of return and under every government make up. However, the third year of a presidential term and a divided government tend to provide the highest average rate of return, which gives us hope for a positive year.

Now for every bad piece of news we can probably find you a positive one that will point to reasons why the market will go up this year. What this just means is we are focusing on quality companies with good cash flow, maintaining our added diversification to commodities and ensuring our clients cash flow needs are protected this year as we might continue to see another volatile year as we manage through the current economic environment.

Congratulations to Rachel!

Join us in congratulating our associate, Rachel Lazewski, in earning the promotion to Senior Client Specialist. The Senior title means she continues to embody Baird’s culture and excel in her role as a client specialist.

Baird Wealth Strategies – Monthly Webinars

Did you know that Baird hosts monthly webinars on a variety of topics, such as market volatility, tax planning topics, insurance and using Baird’s tools?

We call these our Wealth Strategies and they can be found here: https://www.bairdwealth.com/insights/wealth-strategies/

Check out our January Webinar which is discussing Baird’s 2023 Outlook by Strategas.

All Webinars are recorded for later viewing and to keep your inboxes clean we will only send invites to those topics we think are timely and relevant. Be sure to check out the past Webinars.